Right this moment we’ll do a easy run via of a valuation methodology used to estimate the attractiveness of Flutter Leisure plc (LON:FLTR) as an funding alternative by taking the anticipated future money flows and discounting them to at this time’s worth. The Discounted Money Move (DCF) mannequin is the instrument we’ll apply to do that. Do not get postpone by the jargon, the maths behind it’s truly fairly simple.

We usually consider that an organization’s worth is the current worth of all the money it would generate sooner or later. Nevertheless, a DCF is only one valuation metric amongst many, and it’s not with out flaws. If you wish to study extra about discounted money movement, the rationale behind this calculation could be learn intimately within the Simply Wall St analysis model.

Check out our latest analysis for Flutter Entertainment

The Mannequin

We’re utilizing the 2-stage progress mannequin, which merely means we absorb account two levels of firm’s progress. Within the preliminary interval the corporate might have a better progress price and the second stage is normally assumed to have a secure progress price. To begin off with, we have to estimate the following ten years of money flows. The place doable we use analyst estimates, however when these aren’t out there we extrapolate the earlier free money movement (FCF) from the final estimate or reported worth. We assume corporations with shrinking free money movement will gradual their price of shrinkage, and that corporations with rising free money movement will see their progress price gradual, over this era. We do that to replicate that progress tends to gradual extra within the early years than it does in later years.

Typically we assume {that a} greenback at this time is extra useful than a greenback sooner or later, so we low cost the worth of those future money flows to their estimated worth in at this time’s {dollars}:

10-year free money movement (FCF) estimate

| 2023 | 2024 | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 | 2031 | 2032 | |

| Levered FCF (£, Thousands and thousands) | UK£776.7m | UK£1.11b | UK£1.51b | UK£1.77b | UK£1.95b | UK£2.10b | UK£2.22b | UK£2.31b | UK£2.39b | UK£2.45b |

| Progress Fee Estimate Supply | Analyst x12 | Analyst x11 | Analyst x3 | Analyst x1 | Est @ 10.44% | Est @ 7.61% | Est @ 5.62% | Est @ 4.23% | Est @ 3.26% | Est @ 2.58% |

| Current Worth (£, Thousands and thousands) Discounted @ 8.2% | UK£718 | UK£949 | UK£1.2k | UK£1.3k | UK£1.3k | UK£1.3k | UK£1.3k | UK£1.2k | UK£1.2k | UK£1.1k |

(“Est” = FCF progress price estimated by Merely Wall St)

Current Worth of 10-year Money Move (PVCF) = UK£12b

We now must calculate the Terminal Worth, which accounts for all the longer term money flows after this ten yr interval. The Gordon Progress method is used to calculate Terminal Worth at a future annual progress price equal to the 5-year common of the 10-year authorities bond yield of 1.0%. We low cost the terminal money flows to at this time’s worth at a price of fairness of 8.2%.

Terminal Worth (TV)= FCF2032 × (1 + g) ÷ (r – g) = UK£2.5b× (1 + 1.0%) ÷ (8.2%– 1.0%) = UK£34b

Current Worth of Terminal Worth (PVTV)= TV / (1 + r)10= UK£34b÷ ( 1 + 8.2%)10= UK£16b

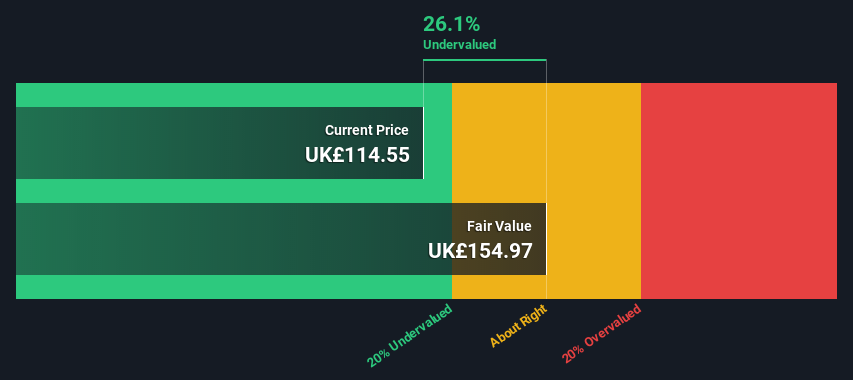

The overall worth, or fairness worth, is then the sum of the current worth of the longer term money flows, which on this case is UK£27b. To get the intrinsic worth per share, we divide this by the entire variety of shares excellent. Relative to the present share worth of UK£115, the corporate seems a contact undervalued at a 26% low cost to the place the inventory worth trades presently. Bear in mind although, that that is simply an approximate valuation, and like all complicated method – rubbish in, rubbish out.

Necessary Assumptions

We’d level out that an important inputs to a reduced money movement are the low cost price and naturally the precise money flows. You do not have to agree with these inputs, I like to recommend redoing the calculations your self and taking part in with them. The DCF additionally doesn’t take into account the doable cyclicality of an trade, or an organization’s future capital necessities, so it doesn’t give a full image of an organization’s potential efficiency. On condition that we’re Flutter Leisure as potential shareholders, the price of fairness is used because the low cost price, relatively than the price of capital (or weighted common value of capital, WACC) which accounts for debt. On this calculation we have used 8.2%, which is predicated on a levered beta of 1.103. Beta is a measure of a inventory’s volatility, in comparison with the market as a complete. We get our beta from the trade common beta of worldwide comparable corporations, with an imposed restrict between 0.8 and a couple of.0, which is an affordable vary for a secure enterprise.

SWOT Evaluation for Flutter Leisure

- Internet debt to fairness ratio under 40%.

- Curiosity funds on debt will not be nicely coated.

- Anticipated to breakeven subsequent yr.

- Has enough money runway for greater than 3 years primarily based on present free money flows.

- Good worth primarily based on P/S ratio and estimated truthful worth.

- Debt is just not nicely coated by working money movement.

Trying Forward:

Though the valuation of an organization is necessary, it is just one of many components that you have to assess for a corporation. DCF fashions will not be the be-all and end-all of funding valuation. As an alternative one of the best use for a DCF mannequin is to check sure assumptions and theories to see if they’d result in the corporate being undervalued or overvalued. If an organization grows at a special price, or if its value of fairness or danger free price adjustments sharply, the output can look very totally different. Can we work out why the corporate is buying and selling at a reduction to intrinsic worth? For Flutter Leisure, we have put collectively three related objects you need to additional look at:

- Dangers: We really feel that you need to assess the 1 warning sign for Flutter Entertainment we have flagged earlier than investing within the firm.

- Administration:Have insiders been ramping up their shares to benefit from the market’s sentiment for FLTR’s future outlook? Try our management and board analysis with insights on CEO compensation and governance components.

- Different Excessive High quality Alternate options: Do you want a superb all-rounder? Discover our interactive list of high quality stocks to get an concept of what else is on the market you could be lacking!

PS. Merely Wall St updates its DCF calculation for each British inventory each day, so if you wish to discover the intrinsic worth of every other inventory simply search here.

Valuation is complicated, however we’re serving to make it easy.

Discover out whether or not Flutter Leisure is probably over or undervalued by trying out our complete evaluation, which incorporates truthful worth estimates, dangers and warnings, dividends, insider transactions and monetary well being.

Have suggestions on this text? Involved concerning the content material? Get in touch with us straight. Alternatively, electronic mail editorial-team (at) simplywallst.com.

This text by Merely Wall St is basic in nature. We offer commentary primarily based on historic information and analyst forecasts solely utilizing an unbiased methodology and our articles will not be meant to be monetary recommendation. It doesn’t represent a suggestion to purchase or promote any inventory, and doesn’t take account of your aims, or your monetary state of affairs. We intention to carry you long-term targeted evaluation pushed by elementary information. Notice that our evaluation might not issue within the newest price-sensitive firm bulletins or qualitative materials. Merely Wall St has no place in any shares talked about.

Source link